Weekly Market Commentary, February 4, 2020

The Markets

The coronavirus continued to spread in China and around the world. Concerns about the virus and measures to prevent its spread will likely reduce economic activity in the first quarter. Interest rates moved lower, and the 10-year Treasury bond yield moved below short-term rates, which indicates concern about the strength of economic growth.

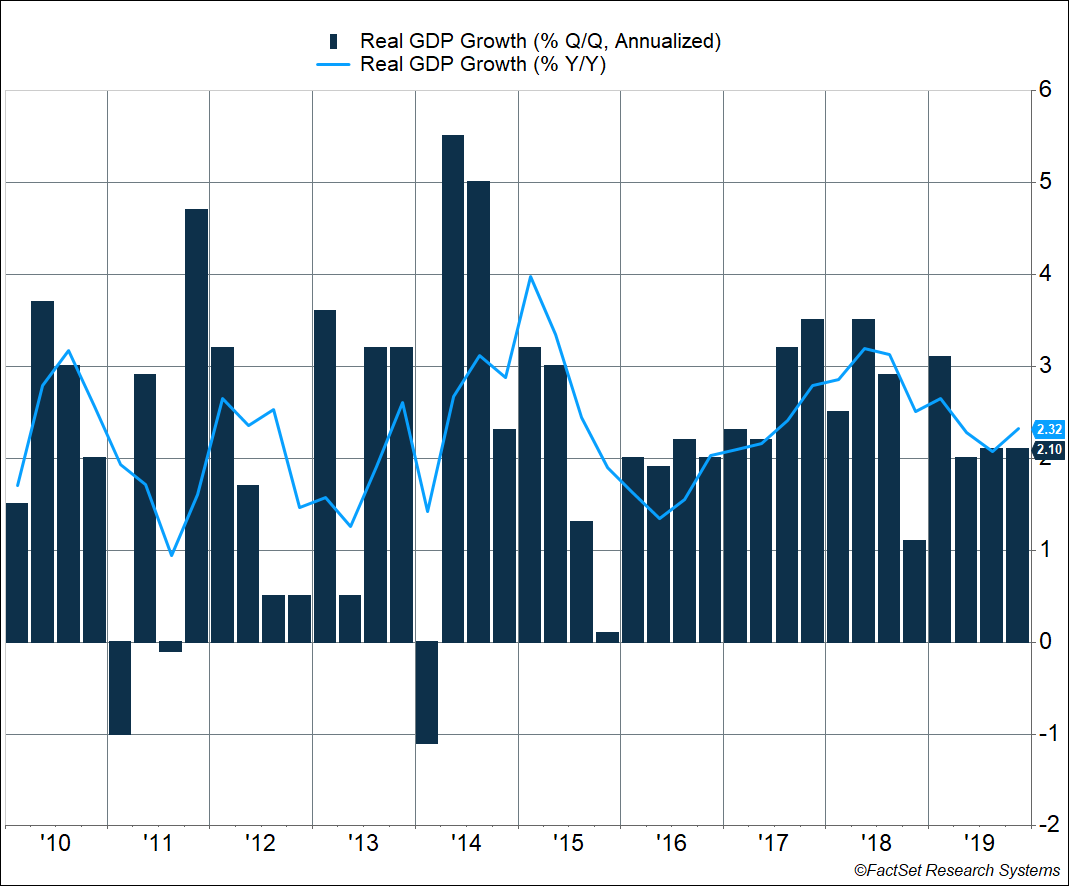

A spate of U.S. economic data painted a picture of an economy that is growing steadily, but not quite as strong as the Federal Reserve would like. U.S. gross domestic product (GDP) rose 2.1 percent last quarter and 2.3 percent in 2019. As the accompanying chart shows, GDP has slowed from peak levels in 2018. Consumer spending and income rose 0.2 percent and 0.3 percent, respectively, dipping from more robust levels. Core inflation rose 1.6 percent, and a broad measure of employee compensation rose 2.7 percent. The Fed targets core inflation of 2 percent and compensation growth above 3 percent would be reflective of the overall economic trends.

Investors focused more on concerns about the coronavirus than the decent economic data. The S&P 500 slid 2.1 percent last week and moved by 1 percent three different times. The last 1 percent move was in October. Global stocks, with greater exposure to China, dropped slightly more. The MSCI ACWI fell 2.5 percent. Bond prices rose in response to the decline in rates. The Bloomberg BarCap Aggregate Bond Index added 0.6 percent to last week’s gains.

Next week may include a State of the Union address, a vote on whether the president stays in office, and the first time Democrats have an opportunity to vote on who their party will nominate for president. Yet, the ability to contain a virus on the other side of the world may garner more attention than all the domestic political events combined.

Data as of 1/31/20 | 1-Week | Y-T-D | 1-Year | 3-Year | 5-Year | 10-Year |

Standard & Poor's 500 (Domestic Stocks) | -2.1% | -0.2% | 19.3% | 12.3% | 9.8% | 11.5% |

Dow Jones Global ex-U.S. | -3.1 | -2.7 | 7.2 | 5.0 | 2.6 | 2.9 |

10-year Treasury Note (Yield Only) | 1.5 | NA | 2.6 | 2.5 | 1.7 | 3.7 |

Gold (per ounce) | 1.3 | 4.0 | 19.7 | 9.3 | 4.5 | 3.8 |

Bloomberg Commodity Index | -3.2 | -7.5 | -7.3 | -5.1 | -5.9 | -5.4 |

S&P 500, Dow Jones Global ex-US, Gold, Bloomberg Commodity Index returns exclude reinvested dividends (gold does not pay a dividend) and the three-, five-, and 10-year returns are annualized; and the 10-year Treasury Note is simply the yield at the close of the day on each of the historical time periods. Sources: Yahoo! Finance, MarketWatch, djindexes.com, London Bullion Market Association. Past performance is no guarantee of future results. Indices are unmanaged and cannot be invested into directly. N/A means not applicable.

Bouncing Back after a Difficult Challenge

Markets are reacting quickly to concerns the tragic loss of life from the coronavirus will continue. Store closures, factory shutdowns, and travel restrictions have all been implemented to contain the virus. Those same actions are reducing economic activity, especially in China. In response, interest rates have dropped and the price of oil moved sharply lower as the slowdown in activity in China will spill over to the rest of the world.

The degree to which the economic slowdown can be contained will depend on a number of factors. The most important will be China’s ability to identify carriers of the virus, find ways to reduce the spread, and improve medicines to reduce the loss of life. For the sake of those infected or at risk, we wish for rapid success.

During declines like this one, consumers and businesses step back purchases, rightly putting more importance on health and safety than economic production. Some of those purchases may be made up in coming weeks, and some may be lost. Below is a list of five types of goods and notes on whether they will likely be made up for or lost:

- Clothing: Clothing is a good example of a purchase that will be pushed to a future period, but not lost. Clothes will still wear out or no longer fit, and fashions will still change.

- Retail goods: Chinese manufacturers will likely experience delays in producing goods for export. Inventories will absorb some of the delay. Once those run out, customers will either delay offering goods or switch to a manufacturer in a different region. When a switch is made, China loses economic activity, but the other manufacturer picks it up.

- Groceries: People need to eat. A return to purchases will likely come as consumers will be forced to return to stores. It is a safe assumption some of those Chinese consumers will switch from shopping at open-air markets, like the one where the disease began, to indoor stores. Again, relatively little loss in overall purchases, but some delay.

- Coffee: Starbucks closed half its stores in China relatively quickly after the outbreak of the virus. When employees return to work, customers will likely return to the coffee shop, too. But, the missed lattes won’t be made up. Many service businesses will endure short-term losses in economic activity.

- Travel: The rise of the virus during the Chinese New Year complicates the analysis of travel. The health concerns came during a busy travel period in China. Many workers have a week or more off work, and returning home is a popular choice. Work schedules will likely mean many of these trips have been cancelled. International airlines have cancelled many flights. Some of those visits will be rescheduled, but others will be lost.

Markets have reacted sharply to the spread of the coronavirus. Part of the reaction is a general concern in the face of uncertainty. Another is the worry the economic activity being lost will not be made up.

Based on the analysis of different transaction types, many transactions will still occur but will be delayed or possibly moved to another region. Other activities will be lost. The global economy is just beginning to recover from a trade war and the long argument over Brexit. The coronavirus has made that recovery more difficult. Our primary wishes and prayers are for quick and healthy recoveries and better medical care. Our secondary concerns are about lost economic growth, a key reason markets have become more volatile.

Reader Questions

[The first quarter provides us a number of opportunities to interact with some of our readers. For the next month, we’ll share some of the questions we get from readers.]

What new risks have you added to your list of concerns?

Last quarter, we experienced a significant drop in uncertainty. U.S.-China trade, North American trade, Federal Reserve policy, and Brexit all made big strides toward clarity. The reduction of uncertainty created an opening for a new risk to join our list of top five concerns.

“Innovation over safety” is our new top-five risk. The tragedies surrounding the Boeing 737 MAX represent the most pointed examples of companies focused on innovation over safety. The risk also encompasses social media companies that control so much of our personal information. Social media companies have grown from small startups to some of the most valuable powerhouses in the world. Any missteps can move markets.

Additional questions about the market? Drop us a line!

Sources:

https://www.ft.com/content/b8027b84-4514-11ea-aeb3-955839e06441 (or go to https://peakcontent.s3-us-west-2.amazonaws.com/+Peak+Commentary/02-03-20_FinancialTimes-Apple_Shuts_42_China_Retail_Stores_Due_to_Coronavirus-Footnote_3.pdf)

https://www.ft.com/content/f3fcdc5a-4119-11ea-bdb5-169ba7be433d (or go to https://peakcontent.s3-us-west-2.amazonaws.com/+Peak+Commentary/02-03-20_FinancialTimes-The_Impact_of_Coronavirus_Across_Industry_and_Finance-Footnote_4.pdf)

https://www.economist.com/international/2020/01/30/chinas-coronavirus-semi-quarantine-will-hurt-the-global-economy (or go to https://peakcontent.s3-us-west-2.amazonaws.com/+Peak+Commentary/02-03-20_TheEconomist-Chinas_Coronavirus_Semi-Quarantine_will_Hurt_the_Global_Economy-Footnote_5.pdf)

https://www.ft.com/content/f3088ca8-43f9-11ea-abea-0c7a29cd66fe (or go to https://peakcontent.s3-us-west-2.amazonaws.com/+Peak+Commentary/02-03-20_FinancialTimes-Eurozone_Grows_Just_0.1_Percent_as_France_and_Italy_Shrink-Footnote_7.pdf)

https://www.insider.com/ways-people-spoil-their-pets-2018-10#they-taught-their-dog-how-to-facetime-1

https://latravelmagazine.com/activities/pet-friendly/

https://www.theodysseyonline.com/14-strangest-things-people-do-with-their-pets

https://www.goodreads.com/work/quotes/44216022-on-cats

https://abcnews.go.com/Business/wireStory/us-economy-grew-moderate-21-rate-fourth-quarter-68637931

https://www.axios.com/coronavirus-starbucks-apple-china-b9a2e48d-3817-45af-9c84-178e79073a5c.html